The Tax Italy Charges on Your American House — Nobody Warns You About This

By Ori Pas | A New Life in Italy

Italy charges an annual wealth tax on your American home if you become an Italian tax resident. Learn how IVIE and IVAFE work, how to calculate them, and how the 7% flat tax regime eliminates them completely.

If your American home is worth $450,000 and you move to Italy — Italy will send you a tax bill for it. Every single year.

Not on the rent it earns. Not on the profit when you sell it. Just for owning it. Nearly $5,000 a year. Like clockwork.

This is called IVIE — Italy's annual wealth tax on real estate you own outside the country. And almost nobody planning a move to Italy knows it exists.

This post covers exactly what it is, how it's calculated, what you can do about it — and how you could pay absolutely nothing.

Who Does This Apply To?

Before going further — this tax is not just for Americans. It applies to anyone who becomes an Italian tax resident — British, Canadian, Australian, anyone. But it hits Americans especially hard (more on that below).

The moment you become an Italian tax resident — meaning you spend more than 183 days a year in Italy — Italy considers your worldwide assets part of your taxable wealth.

What Is IVIE?

IVIE is Italy's annual wealth tax on real estate you own outside the country. The rate is 1.06% of the property's value. Every year.

It doesn't matter if it's sitting empty, rented out, or your kids are living in it. You own it — you pay.

How Is It Calculated — And Why Your Deed Matters

Here's something most people don't know — and it matters a lot.

Italy doesn't automatically use your home's current market value. For US properties, IVIE is calculated on the original purchase price — what you paid for the home, as stated in your purchase deed.

This is actually good news if your home has appreciated significantly. Italy taxes what you paid, not what it's worth today.

But — and this is critical — you need to be able to prove it. If you cannot produce your original purchase deed, Italy will fall back on the current market value. And in most parts of America today, that's significantly higher than what you paid.

Action point: Before you even think about moving — find your deed. Scan it. Save it. Back it up.

That one document could save you thousands of euros every single year.

What Is IVAFE?

IVIE covers real estate. IVAFE covers everything else.

Bank accounts. Brokerage accounts. ETFs. Investment portfolios. If it's a financial asset held outside Italy — Italy charges 0.2% on the value every year.

So your US savings account, your stock portfolio, your ETFs — all of it goes on Italy's radar the moment you become an Italian tax resident.

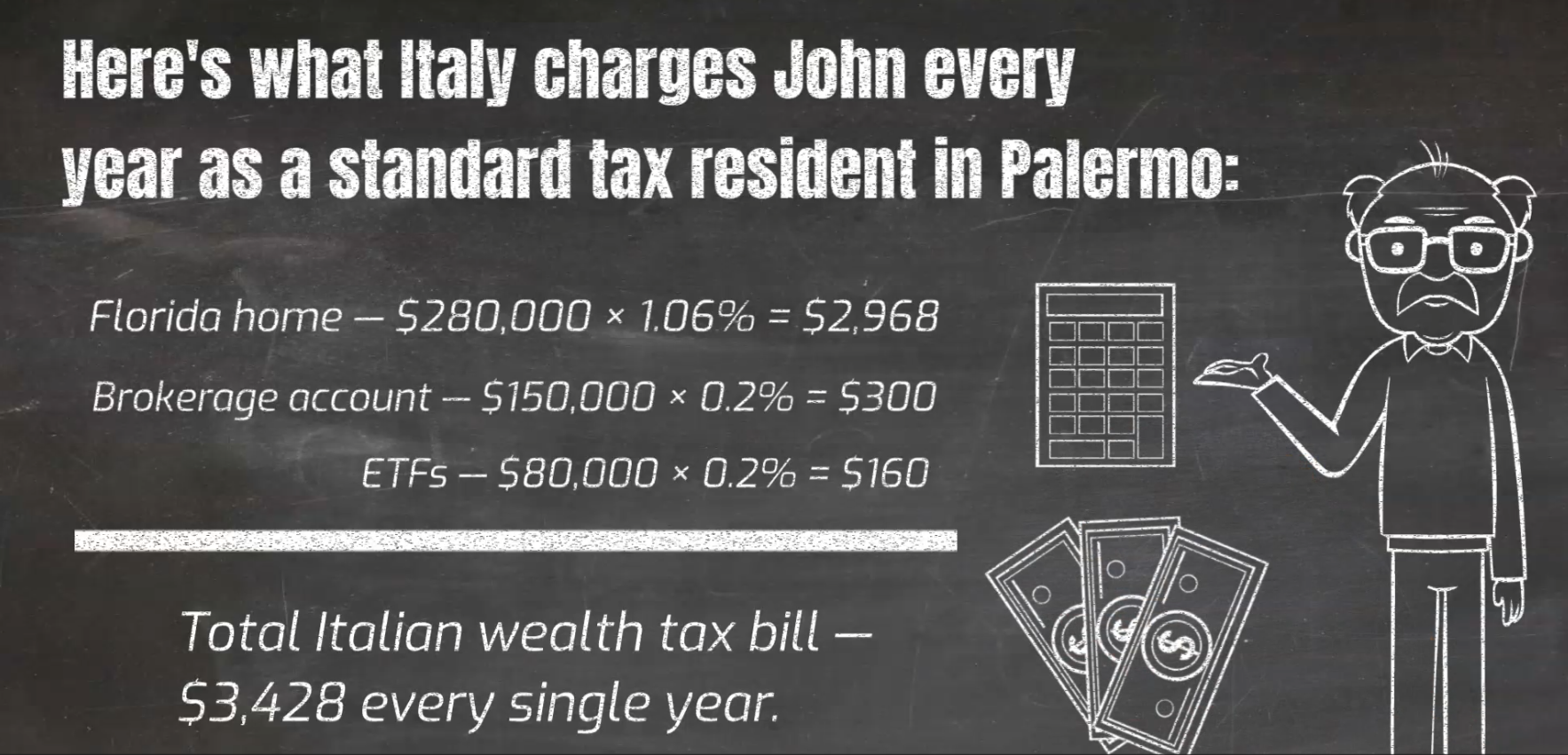

A Real-World Example — Meet John

John is 62, retiring to Palermo, Sicily. He owns a home in Florida worth $450,000 today — but he bought it for $280,000. He kept his deed. He also has $150,000 in a brokerage account and $80,000 in ETFs.

Here's what Italy charges John every year as a standard tax resident:

AssetValueRateAnnual TaxFlorida home$280,0001.06%$2,968Brokerage account$150,0000.2%$300ETFs$80,0000.2%$160Total$3,428/year

Over 10 years of retirement — that's over $34,000.

The 7% Escape Hatch

Here's the most important thing in this entire post.

If you qualify for Italy's 7% flat tax regime — you pay zero IVIE and zero IVAFE. None. For 10 full years.

No wealth tax on your American house. No wealth tax on your brokerage account. No foreign asset reporting at all.

The 7% regime is available to foreign pensioners who move to qualifying towns in southern Italy — towns with under 30,000 residents in regions like Sicily, Puglia, Campania, Calabria, and Abruzzo.

So John — moving to a qualifying town in Sicily — pays zero on his Florida home, zero on his brokerage account, zero on his ETFs. His $34,000 over 10 years becomes nothing.

This is why where you choose to live in Italy isn't just a lifestyle decision. It's a financial decision worth tens of thousands of dollars.

One important note: the 7% regime lasts for 10 years. After that, you pay like everyone else. When that day comes, you'll want to be taxed on your purchase price — not today's market value. Which is why you still need to keep that deed safe, even if you qualify for the regime now.

The Good News — And the American Sting

Even if you don't qualify for the 7% regime, there's still good news.

If you're already paying property tax in the US on your home — and most Americans are — you can use that as a tax credit against your IVIE bill. Because US property tax rates are generally high enough, that credit often cancels out the IVIE entirely.

And if your total IVIE calculation comes to less than €200 — you pay nothing at all.

Here's the extra sting for Americans specifically: unlike most taxes you pay abroad, IVIE and IVAFE cannot be claimed as a Foreign Tax Credit on your US tax return. The IRS considers them wealth taxes, not income taxes.

So for Americans, these are a genuine additional cost with no offset on the US side. Which makes qualifying for the 7% regime — or maximising your US property tax credit — even more important to understand before you move.

Three Things to Do Right Now

1. Find your original purchase deed for every property you own. Scan it. Store it safely. Without it, Italy uses market value — and that's almost always more expensive.

2. Figure out whether you qualify for the 7% flat tax regime. If you're a foreign pensioner moving to southern Italy, this is the single most important tax decision you'll make. It eliminates IVIE, IVAFE, and simplifies everything. Email me at op2001il@gmail.com and I'll connect you personally with the specialist I work with.

3. Download the free Italy Relocation Roadmap. It covers the full financial picture of moving to Italy in plain English. Completely free. 👉 Get the free Roadmap

The Bottom Line

Italy is still one of the best decisions you can make for your retirement. But go in with your eyes open.

IVIE and IVAFE are real. They apply to everyone who becomes an Italian tax resident — regardless of where you're from. But with the right planning, the right documents, and the right location — they can cost you a lot less than you think. Or nothing at all.

Want to Go Deeper?

📖 The Italy Retirement Blueprint — 18 chapters covering taxes, visas, costs and everything you need before you move. 👉 Get the Blueprint — $57

📋 The Italy Elective Residency Visa Guide 2026 — your complete step-by-step ERV application guide. 👉 Get the ERV Guide — $19

👥 Italy Relocation Planning Club — free community, direct access to me. 👉 Join Free